LTV calculator

You can feel comfortable when navigating the world of real estate finance. However, you can calculate loan to value ratios conveniently with the LTV calculator. Make smart investment decisions. In addition, when you understand the relationship between the amount of your loan and the value of the property you are financing.

Furthermore, whether you’re an experienced investor or a first-time homebuyer, make sure you stay informed and in control during real estate transactions with our user-friendly tool.

What is an LTV ratio calculator?

To understand the working, let’s break down the term first.

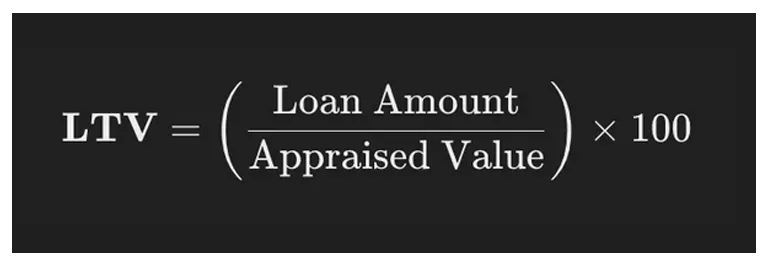

It refers to the loan-to-value ratio. It’s a financial term used among lenders. It measures the loan-to-asset cost ratio.

When you use this calculator, you can calculate the potential risk associated with a mortgage approval. At its core, it is a comparison between the property’s assessed value and the monthly mortgage payment (the original loan amount).

Furthermore, it represents a high or low valuation; a lower ratio often means more favorable contract terms. This loan to value ratio calculator is designed to help you quickly and accurately elaborate on how to figure out LTV equity.

How to Calculate LTV?

To find equity and assess your financial risk is essential when you consider a mortgage or other large installment. Getting the loan to value ratio can allow you to figure out how much equity you have in your property and how much risk you are taking on with a mortgage.

In addition, you can make more informed decisions about the borrowing and potentially save money in the long run. For this purpose, evaluate the property’s assessed worth, divide it by the loan amount, and then multiply the result by 100.

Here’s a quick guide on how to figure out LTV loan calculator for a mortgage or home equity financing.

- Determine the Appraised Value:

An assessment will help you to ascertain the market value of your property. - Identify the Mortgage Payment, Down Payment or Loan Amount:

Subtract your down payment from the appraised worth to find the amount you need to borrow.

Apply the Formula:

Use the formula:

Example: 1

If you put $30,000 down and the home is valued at $150,000, your monthly mortgage payment will be $120,000. The calculation would be:

LTV = (120,000 / 150,000) × 100 = 80%

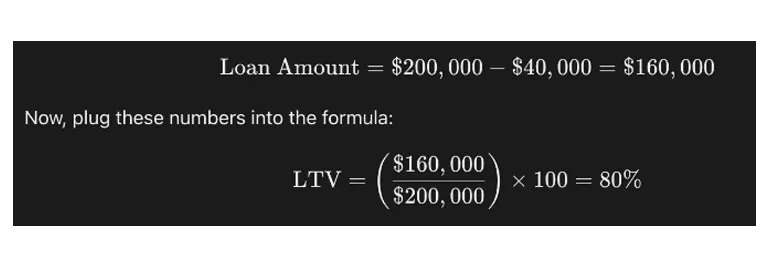

Example: 2

Imagine you are buying a home with an appraised value of $200,000, and you make a down payment of $40,000. This means the borrowed amount you need is:

Our easy-to-use LTV cal module lets you plug in these numbers. This is particularly useful when you’re figuring loan to value ratios for a potential home purchase or refinance.

Factors Affecting Your LTV Ratio

Most of the factors that help in your planning ahead include your credit score, debt-to-income ratio, and the current market conditions. Before you apply for a credit, be sure you know how these things might affect your percentage of equity.

- Appraised Value:

It is directly related to how much your property is worth on the market. When the LTV value is reduced, it shows an increase in the estimated purchase price, which is relative to the financing amount. - Down Payment Amount:

Mortgage payments are actually reduced in relation to the size of the down payment. This has a direct impact on lowering the value of your mortgage. - Mortgage Payment:

It’s basically determined by the amount you borrow. When you want to reduce the monthly mortgage payment. You can either put a larger down payment or negotiate a lower purchase price. Additionally, higher down payments lower mortgage payments. - Additional Financial Factors:

In cases where multiple financial assistance is involved (such as secondary financing), a combined loan-to-value (CLTV) ratio may be used. We still prioritize the standard LTV calculation for most home purchases.

What Is the Impact of a High vs. Low LTV Calculator Ratio?

High LTV: Pros and Cons

It means you’re borrowing more of the property’s value. But there are some important considerations to keep in mind:

- Restrictive Loan Conditions:

Many lenders consider high LTVs risky. As a result, capital offers may be less appealing, and interest rates may rise.

Low LTV: The Advantages

A lower LTV generally reflects a strong financial position:

- Better Credit Offers:Lenders offer better terms and rates.

- Reduced Financial Risk:

Your upfront investment lowers the lender’s risk and your long-term financial burden. - Stronger Negotiation Leverage:

Allow you to negotiate better terms with your lender.

- Higher Monthly Payments:

Due to the increased amount you are financing, the monthly mortgage payment is likely to be higher. - Limited Negotiation Power:

The best deals may be unavailable to high-LTV borrowers. Our calculator LTV ratio can help you determine how much you’ll need to borrow and how it may affect funding.

Tips for Lowering Your LTV Ratio

Consider these options if you find that your LTV is higher than you’d like it to be:

- Increase Your Down Payment:

The deposit amount and LTV can be decreased. When you increase the amount you contribute from your own resources. This is a simple and effective way to boost your finances. - Negotiate the Purchase Price:

Retaining the initial investment at a lower property price can lead to a better lease-to-value ratio. - Improve Your Credit Profile:

Although a good credit score might not directly reduce your mortgage worth. You can get better credit terms and lower costs with it. - Monitor Appraisal Values:

Consider a second appraisal if you think your property is undervalued. When the property is worth more than you thought, a good appraisal is needed.